TL;DR: Your net settlement depends on the deductions taken from the total amount, including attorney fees, case costs, medical liens, and any other required payments. Review your fee agreement and settlement statement to understand what you may actually receive.

Highlights:

- Get a copy of your signed contingency fee agreement and any rate increases.

- Confirm whether the attorney’s fee is calculated on the gross or net recovery.

- Request an itemized breakdown of case costs before you approve disbursement.

- Gather and review all medical lien or reimbursement notices tied to treatment.

- Ask your lawyer whether California Civil Code 3040 limits apply to your liens.

- Review the settlement statement for potentially taxable items, such as interest or punitive damages.

- Budget for delays after signing the release, especially with Medi-Cal or Medicare liens.

Tip: Save copies of bills, EOBs, lien letters, and the signed release, and stick to documented facts when discussing deductions.

Table of Contents

If you’re wondering how much of a $100,000 settlement you might actually receive, the answer depends on the details of your case. Attorney fees, case costs, and medical liens can reduce the settlement amount before you receive any money.

For example, a $100,000 settlement with a 33⅓% attorney fee, $5,000 in case costs, and $15,000 in medical liens may leave about $46,667 before any other deductions. This is only a sample calculation, not a prediction. Your actual net recovery depends on your fee agreement, case costs, lien amounts, settlement terms, and any taxable portions of the recovery.

Waiting for a settlement to close is stressful, especially when medical bills keep arriving. Worrying about your financial stability on top of recovering from an injury is a heavy burden. Not knowing your net payout makes that uncertainty even harder to handle. Understanding the math can give you a clearer sense of where you stand.

Each deduction follows its own rules, and those rules can move your final number significantly. You can find the settlement deductions on a settlement statement, but the order can vary by fee agreement.

Many firms calculate the contingency fee on the gross recovery, then reimburse case costs, then address liens and reimbursements. Other agreements may handle these deductions differently, so you should review your written fee agreement and settlement statement carefully.

You can negotiate some of those amounts before the case closes. That is why two people with the same $100,000 settlement can walk away with different amounts.

Where Does The Money Go In A $100k Settlement?

A $100,000 settlement does not necessarily mean you will receive a $100,000 check. Various deductions, such as attorney’s fees, case costs, and medical liens, may reduce the amount you ultimately take home. The exact deductions vary from case to case, so the specific facts and expenses involved will determine your net recovery.

Typical settlement deductions include:

- Attorney Fee: Calculated based on the contingency fee percentage agreed to in advance.

- Case Costs: They include litigation and administrative expenses, such as filing fees, record requests, expert witness fees, and other case-related costs.

- Medical Liens: Amounts that a provider, health plan, or government program may claim from the settlement based on payments for your care. The right to recover depends on the payer and the legal basis for the claim. These costs can include emergency care, hospital treatment, physician services, physical therapy, and chiropractic care.

The final amount you receive depends on deductions for attorney’s fees, case expenses, and medical liens. These deductions come out before your settlement reaches you.

How California Attorney Fees Are Calculated

Many clients ask: Do lawyers only get paid if they win? For most injury attorneys, the answer is yes. This is because they often work on a contingency fee basis. Under many contingency fee agreements, you do not owe attorney fees unless there is a recovery. However, your written agreement should explain whether you may still be responsible for case costs.

The fee is a share of what you recover. Your written fee agreement determines the exact rate. The percentage depends on the case’s complexity, but it’s typically around 30% to 40%.

Many California personal injury attorneys charge a lower percentage before a lawsuit is filed. The rate increases once the case moves to court. The higher rate reflects the extra time and risk for the attorney. Your written fee agreement should state the contingency fee percentage. However, the final attorney’s fee depends on the amount recovered.

Lawyers who work on contingency must give you a written fee agreement. Under the California Business and Professions Code, this contract must be in writing and signed by you before or when representation starts. The agreement must set out the fee terms, including any applicable rate.

Case Costs And Expenses Explained

Case costs are the real expenses your attorney pays to build your personal injury claim. They are separate from the attorney’s fee percentage. Think of them as the bills that come with investigating and filing your case. If your case succeeds, your attorney reimburses the case costs from the resulting settlement or award.

Common case costs include:

- Police Reports: The fee to get the official accident report.

- Medical Record Fees: Charges to gather your treatment records and billing history.

- Expert Witness Fees: Payments to doctors, accident reconstruction specialists, or economists who support your claim.

- Court Filing Fees: The fees charged by the court to file your lawsuit and related documents.

Your attorney advances these costs during the case. If your case results in financial compensation, the costs are deducted from your recovery separately from the attorney’s percentage fee.

If you recover compensation, your attorney deducts those costs before paying you the remaining funds. Beyond attorney fees and case costs, other legal obligations may reduce what you take home.

Medical Liens In California Injury Claims

Some medical providers, health plans, and government programs may assert a lien or reimbursement claim against your settlement if they have a legal or contractual right to do so. A lien is a legal claim. It gives someone the right to take a portion of your settlement before the money reaches you.

Depending on the circumstances of the accident, parties who can place a lien on your settlement can be your:

- Primary care doctor

- Hospital

- Treatment specialists

- Health insurers

- Government programs

California law limits how much certain healthcare providers and insurers can recover from an injury settlement. The cap applies to medical expenses paid on your behalf. This rule generally applies to insurers regulated by the California Department of Managed Health Care or the California Department of Insurance.

Not every type of lien is subject to these limits. Medi-Cal, Medicare, workers’ compensation, and hospital liens may follow different rules. A lawyer can review which rules apply to your settlement before any money gets distributed.

These limits can make a significant difference, allowing more of the settlement to remain with the injured person. Thinking, “I need a personal injury lawyer to handle my case,” is a valid thought. If you feel that these liens are unfair, you can have a lawyer negotiate on your behalf.

Are Personal Injury Settlements Taxable?

In many physical injury cases, the IRS does not treat compensatory settlement money as taxable income. The IRS generally does not count this money as income when it compensates you for physical injuries or physical illness. However, taxable portions may still exist, so you should not assume every part of a settlement receives the same tax treatment.

Federal law protects this money under IRC Section 104. Are you still asking, “Is my personal injury settlement taxable?” The answer depends on whether the compensation is tied to physical injuries or includes items like punitive damages or interest.

However, there are certain parts of a claim that can be taxable:

- Punitive Damages: These are extra damages meant to punish the defendant, not to reimburse you for your losses.

- Interest: Interest that builds up on your settlement before you receive it may also be taxable.

- Non-Physical Injury Damages: Some damages not tied to a physical injury may be taxable, depending on the settlement structure.

While taxes typically do not apply to physical injury compensation, every settlement has its own variables.

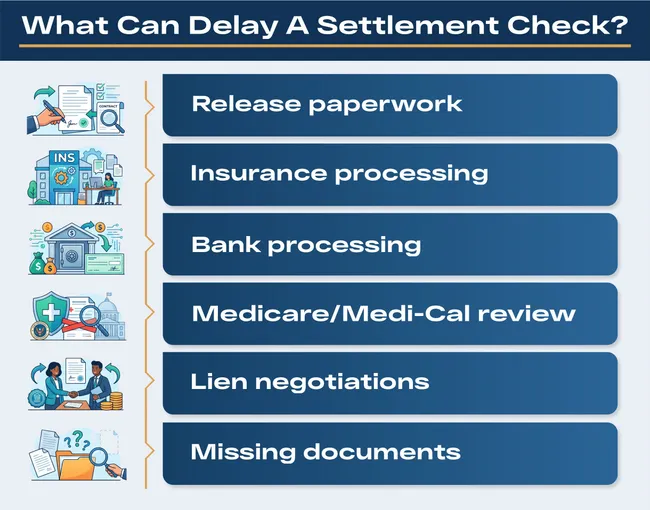

How Long Until The Settlement Check Arrives?

There is no fixed deadline for when a settlement check must arrive. Many cases fund within weeks after the signed release, but liens, insurer processing, and check issuance can extend the timeline. Your case may resolve faster or take longer, depending on its specific details.

If Medi-Cal or Medicare paid for any of your treatment, lien negotiations can push your timeline well past 60 days. For Medi-Cal liens, the lien process can depend on the settlement date, the final date of treatment, provider billing, and the agency’s review timeline. Government health liens alone can add months to your wait.

Before you sign anything, it is advisable to review everything. Some people seek free advice from a personal injury attorney to understand the timeline for getting their settlement. An attorney can explain potential delays, review the deductions, and assess whether the timeline appears reasonable based on the facts of the case.

Frequently Asked Questions

Settlement calculations can be hard to follow. The stakes are high when you are hurt and waiting to see what compensation may be available in your case. Below are answers to common questions victims ask about these matters.

What Is A Reasonable Personal Injury Settlement In California?

A reasonable settlement should account for your losses, including medical bills, lost income, future care needs, and pain and suffering. The amount depends on your injuries, who caused the crash, what evidence supports your claim, and what insurance is available.

How Long Does It Take To Reach A Personal Injury Settlement In California?

Cases with clear fault and completed medical treatment can wrap up in a few months. Cases with serious injuries or disputed fault can take a year or more. The harder the case, the longer it takes to resolve.

What Happens If A Personal Injury Settlement Involves Medi-Cal?

Medi-Cal generally has the right to recover for injury-related care it paid for. Your lawyer can dispute unrelated charges and request reductions when allowed under Medi-Cal rules. These lien issues can affect both your final net recovery and the time it takes to receive your settlement funds.

What If The At-Fault Party Has Low Insurance Limits Or No Insurance?

Your own uninsured/underinsured motorist coverage may help cover the gap if your policy includes it. It can help pay the difference between the other driver’s limit and your actual losses, up to your own UM/UIM policy limits. Without UM/UIM coverage, you may only collect what the at-fault party can pay out of pocket.

Should I Accept The First Settlement Offer?

In most cases, it is not advisable to accept the first settlement offer. Early offers are often lower than the full value of a claim and may not reflect future medical care, lost income, or long-term effects. A settlement release is a legal document that ends your right to seek further compensation for the same injury. Once it is signed, the claim is generally considered fully resolved.

Get Legal Help From Arash Law

Our injury attorneys at AK Law know how settlement deductions work under California law. We understand how liens and fees affect your final payout. When you contact us, our lawyers can review your situation and walk through your options. Call (888) 488-1391 for a free initial consultation to learn what deductions may apply to your settlement and what your potential net recovery could look like based on your specific case.