TL;DR: If you get into a car accident in a different state, local laws may differ depending on the state. This may affect your insurance coverage, fault determination, and legal procedures. Be aware of how state-specific negligence laws and insurance policies impact your claim.

Highlights:

- The laws of the state where the accident occurred will apply to your case.

- At-fault states hold the driver responsible for damages caused by the crash.

- No-fault states require filing claims with your own insurance, regardless of fault.

- Negligence laws vary by state, affecting your ability to recover damages.

- Auto insurance coverage, including PIP and UM/UIM, varies by state.

- Consulting a personal injury lawyer can help you navigate out-of-state accident laws.

Tip: Ensure your insurance covers out-of-state accidents and meets local requirements.

Table of Contents

After a car accident outside of California, the laws of the state where the crash occurred generally cover the resulting claim. Courts may use choice-of-law principles to determine jurisdiction. Meanwhile, insurance disputes often center on policy wording and accident location.

The laws governing car accidents and personal injury claims vary from state to state. For instance, California follows an at-fault system, which places financial responsibility for the victim’s losses on the driver who caused the accident. It also upholds pure comparative negligence laws, which allow injured victims to pursue compensation even if they’re up to 99% responsible for the crash.

However, other states may not follow these rules. If your car accident occurs in another part of the country, certain distinctions can affect who is liable and the damages available in your case.

Legal Rules That Apply In Out-Of-State Car Accidents

The laws of the state where the car accident occurred apply. That can influence how out-of-state insurance coverage applies and how lawyers, insurers, and courts assess liability. Generally, auto policies cover car accidents nationwide. Your insurer may adjust your policy limits to a state’s specific minimums.

If a claim proceeds to litigation, the courts of the state where the crash occurred typically have jurisdiction and can hear the case. A lawsuit may sometimes be filed where the defendant lives if that court has personal jurisdiction. However, in out-of-state car accidents involving drivers from different parts of the country, choice-of-law principles determine which laws apply. To illustrate, consider this scenario:

- You, a driver from California, get involved in a car accident while visiting Las Vegas.

- If you sue the other driver, you may have to submit your case to a Nevada court. The lawsuit is often filed in the state where the crash occurred.

- Under choice-of-law principles, California laws may apply because your insurance policy is based in California.

Finally, a state’s fault system can influence the outcome of a claim or lawsuit:

- In at-fault states, whoever caused the crash must cover the victim’s damages. An injured party usually files a claim against that driver’s auto insurance policy.

- In no-fault insurance states, drivers must carry personal injury protection coverage. This policy may cover medical bills and lost wages, depending on the state. It applies regardless of who caused the car accident.

Understanding Fault Insurance Laws By State

Car accident insurance laws in the U.S. fall into two main categories: at-fault and no-fault systems. Which one applies depends on the state where the crash happened. This distinction influences how and where victims can file a case.

In at-fault states, victims may file a claim against the other driver’s liability coverage. Conversely, injured parties in no-fault states seek compensation from their own personal injury protection (PIP) insurance. No-fault systems also restrict lawsuits unless they meet specific legal requirements.

Here’s how the two systems typically determine liability:

- At-Fault States: The party who caused the accident is liable. Claims usually go through the at-fault driver’s insurance policy. The goal of a claim is to help the victim recover compensation for financial and intangible losses.

- No-Fault States: Each party involved in an accident files a claim with their own insurer. That allows them to seek compensation regardless of who was at fault. This system can make things complex, especially if you come from a state with a fault-based system.

Three states, namely Pennsylvania, Kentucky, and New Jersey, implement a hybrid system called “choice no-fault.” Drivers may choose whether their policy follows the no-fault or at-fault system. If no option is selected, the state’s default system applies:

- At-fault in Pennsylvania.

- No-fault in Kentucky and New Jersey.

How Do State Negligence Laws Influence A Personal Injury Lawsuit?

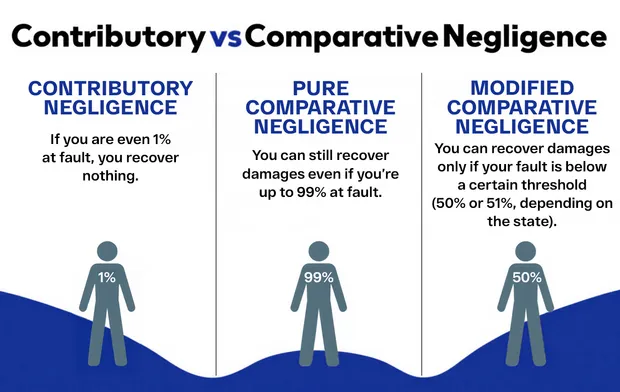

Negligence systems determine whether an injured victim can still pursue compensation if they contributed to the crash. California follows pure comparative negligence rules, while other states may apply contributory or modified comparative negligence. In some cases, the differences between these systems completely bar victims of out-of-state car accidents from recovering damages through a lawsuit.

Below is a quick overview of the negligence rules applied across the country:

- Contributory Negligence: A plaintiff must be completely free of liability to recover any damages.

- Pure Comparative Negligence: A plaintiff can still seek compensation, even if they’re up to 99% at fault. However, courts can reduce their compensation by the percentage of liability assigned to them.

- Modified Comparative Negligence: This system is similar to pure comparative negligence. However, a plaintiff’s liability must not surpass 50% or 51%, depending on the state.

How Out-Of-State Auto Insurance Works

Many car insurance policies have a broadening clause. Policies typically cover the U.S., Canada, and territories. Under it, insurers may raise coverage to match higher minimum liability limits in other states. However, policy wording may affect how this clause applies. Additionally, PIP insurance policies, as well as the terms and conditions for uninsured/underinsured motorist (UM/UIM) coverage, vary by state and endorsement.

Here’s how different components of auto insurance may apply after an out-of-state car accident:

Broadening Clauses

The location of a crash can influence how car insurance coverage applies. Some policies have a “broadening clause.” That means they will automatically provide the minimum coverage limits required by the state where the accident occurred.

Uninsured/Underinsured Motorist Coverage

UM coverage protects you in accidents with drivers who lack insurance. Laws on uninsured drivers vary from one place to another. For example:

- Uninsured Motorist Bodily Injury (UMBI) coverage applies to medical costs, lost wages, and pain and suffering for drivers, their passengers, and their family members if they’re injured in a crash. Approximately 20 to 22 states, as well as the District of Columbia, require drivers to carry UMBI coverage. Minimum limits vary per state.

- Uninsured Motorist Property Damage (UMPD) coverage may pay for vehicle repairs up to policy limits. In some states, it comes with a deductible.

Underinsured motorist (UIM) coverage can be used in case the at-fault driver’s insurance isn’t enough to pay for all of your damages.

- Underinsured Motorist Bodily Injury (UIMBI) coverage applies when the other driver has insufficient insurance limits for your injuries. It can cover lost wages, medical expenses, and pain and suffering.

- Underinsured Motorist Property Damage (UIMPD) coverage may step in after crashes involving drivers with inadequate coverage for your car’s repair or replacement.

Though some states require drivers to carry these coverages, others don’t. For instance, insurers in California are required to offer UM/UIM coverage. However, policyholders may waive them in writing.

Insurance Coverage For A Rental Car

Many rental car companies offer supplemental insurance. A Collision Damage Waiver (CDW) may assist you if someone damages your rental car. It can cover repair or replacement costs, depending on your rental agreement. These policies can overlap with your personal car insurance coverage. The other driver’s policy or your own may take effect if you didn’t get a rental car insurance policy.

Here are a few things to keep in mind:

- Certain credit cards offer secondary coverage. These provide extra protection if you use them for the rental reservation.

- State minimums still apply. That means your coverage must at least meet the local insurance requirements.

Common Injuries In Out-of-State Car Accidents

Car accidents that cross state lines can cause injuries that vary from minor to severe. Seeking medical help in an unfamiliar location can be challenging. Victims usually suffer bruises, sprains, and strains. Some may sustain more severe injuries, such as head trauma and whiplash.

Some catastrophic injuries in out-of-state car accidents include:

- Traumatic Brain Injuries (TBIs): Victims may sustain head trauma if they hit hard surfaces, such as steering wheels, during a crash. These injuries can result in a decline in mental ability, adversely affecting quality of life. Victims may need long-term care or assistive devices to recover. Extreme cases may lead to fatalities.

- Spinal Cord Injuries: Damage to the spine can lead to permanent disability. Victims may suffer partial or complete paralysis. Others might only need rehabilitation, including physical therapy and chiropractic care.

- Burns: These injuries can result from contact with hot surfaces and open flames. After a car crash, victims may suffer permanent scarring or disfigurement. Some may develop a dependency on pain medication.

- Lacerations: Severe cuts are common after a serious car crash. Deep lacerations may cause scarring, disfigurement, chronic pain, and nerve damage.

Aside from physical injuries, a car accident may also cause mental health issues. Some victims may suffer anxiety, depression, and post-traumatic stress. Some may need visits with a therapist.

How A Personal Injury Lawyer Helps With Out-Of-State Claims

Car accident lawyers can provide legal representation for accidents across state lines. In many cases, an attorney may participate in an out-of-state case through a process called pro hac vice admission, which usually requires partnering with a lawyer licensed in that state and obtaining court approval. That means they can help out-of-state car accident victims by working with local contacts, answering calls, and filing paperwork. In many cases, they can help even if they are not in the state where the collision occurred.

In this capacity, a personal injury attorney can also:

- Provide car accident legal advice to clients.

- Help victims navigate another state’s accident reporting procedures.

- Collect evidence, such as medical records and police reports.

- Keep track of state-specific timelines and filing requirements.

- Review insurance policies and assess coverage.

- Communicate and negotiate with insurance adjusters.

- Handle insurance dispute resolution.

Interstate accident claims may require coordination with lawyers licensed in the state where the crash occurred. Local counsel may handle court filings and hearings while the primary attorney manages case strategy and client communication.

Frequently Asked Questions About Car Accidents In A Different State

A car crash in a different state raises many questions about liability. Getting clear answers can help victims decide how to proceed with their claim. Below are some of the most frequently asked questions about out-of-state car accidents.

How Much Will My Insurance Go Up By After An Accident?

Compared to other motorists, drivers who cause a crash may see their car insurance rates increase by roughly 48%. This estimate is based on a nationwide NerdWallet analysis published in 2026. The exact percentage depends on the specifics of a case.

The exact amount your insurance may go up depends on several factors:

- Your Insurance Carrier: Each company assesses risk differently.

- Severity of the Accident: Severe collisions can significantly affect your premiums.

- Your Driving History: Previous incidents on your driving record influence your rates.

- Accident Forgiveness: Some policies won’t increase premiums for the first at-fault accident.

Some states have laws in place to protect consumers from unfair rate hikes. For instance, California’s Insurance Commissioner must approve an insurer’s filed rate before a hike goes into effect. This process is governed by Proposition 103.

What Happens If I Go To The ER In A Different State?

You are still covered if you visit an out-of-state emergency room. The federal No Surprises Act protects consumers from certain unexpected medical expenses. These include most emergency and post-stabilization services from an out-of-network provider. It may also cover some non-emergency care and air ambulance services.

If you’re from California, here are some things to consider when visiting an ER after an out-of-state car accident:

- Medi-Cal covers emergencies nationwide. Non-emergency care outside the state is excluded unless approved by the insurer.

- Private plans vary depending on the terms of the policy.

- Health Maintenance Organizations (HMOs) offer lower premiums and out-of-pocket expenses. However, they require using in-network physicians and obtaining referrals for specialists.

- PPOs (Preferred Provider Organizations) offer greater flexibility by allowing direct access to specialists and coverage for care outside the network. Notably, they also come with higher premiums and out-of-pocket costs.

How Many States Follow An At-Fault System?

Most states (38 out of 50) follow an at-fault system. These include California, plus the District of Columbia. Only 12 states follow a no-fault system (three of those are “choice no-fault”).

How Long Do I Have To File An Out-Of-State Car Accident Lawsuit?

It depends on the statute of limitations in the state where the crash occurred. Some only give motor vehicle accident victims one year to file a civil case. Others impose a more lax three-year limit. However, the deadline to sue is two years in most states.

Some exceptions may apply. For example, California pauses the statute of limitations for victims under 18. Deadlines may also be shorter when a claim is filed against a government entity. Consulting a lawyer can help you learn which deadlines apply to your case.

Do Lawyers Only Get Paid If They Win My Out-of-State Car Accident Claim?

Yes, if you get legal representation on a contingency fee basis. Under this arrangement, you only pay your lawyers if they win your case or recover compensation through a settlement.

Do I Need A Personal Injury Lawyer For An Out-of-State Car Accident?

You can file a car accident claim without hiring a personal injury lawyer. However, legal procedures vary by state, which can make the process confusing. A car accident lawyer can clarify any legal and insurance differences and offer personalized guidance. They also handle complex issues in interstate cases.

What Are Recoverable Damages In An Out-Of-State Car Accident?

Depending on the facts of your case, you may file a claim for the following types of damages after an out-of-state car accident:

- Economic Damages: These account for monetary losses, such as:

- Medical costs

- Lost wages

- Property damage

- Non-Economic Damages: These compensate for intangible losses, including:

- Pain and suffering

- Loss of companionship

- Diminished quality of life

- Punitive Damages: These may be available in rare cases. Laws surrounding them vary significantly across different states. In California, you need clear and convincing proof of malice, fraud, or oppression.

Seek Guidance For An Out-Of-State Car Accident Case

An out-of-state car accident presents unique legal challenges. Understanding liability laws and the steps for settling car accident claims can help.

You may be looking for free car accident lawyer advice online. At Arash Law, we provide free initial consultations. Our attorneys can review your case and answer your questions. We can help you make informed decisions about your out-of-state car collision claim.

Our personal injury lawyers have recovered over $1 billion for clients. We work on a no-win, no-fee basis. That means we won’t charge you legal fees unless we recover compensation for you. Reach out to our team at AK Law today.

Call us at (888) 488-1391 for a free case review. You can also fill out our “Do I Have A Case?” form.